Documents and digital data, unified: A faster path to consumer lending decisions

Consumer lenders face a simple mandate that is hard to execute: approve more good borrowers faster without loosening controls. Borrowers expect to apply on a phone and get near-instant answers. The most reliable way to deliver both is to unify documents with digital connections so each file tells one clear, corroborated story.

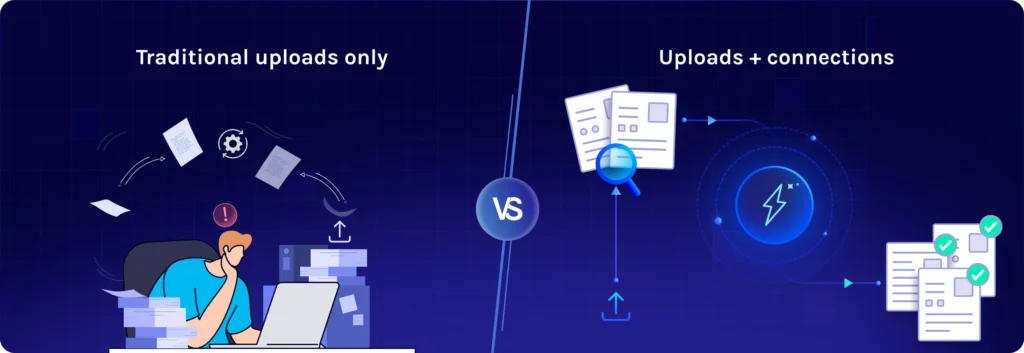

What we mean by documents and digital connections

Documents are the familiar artifacts applicants upload — pay stubs, W-2s, government IDs and bank statements. Digital connections are permissioned links to the same underlying evidence, shared directly from sources the borrower controls, such as connecting a bank account through a provider like Plaid or verifying employment through an approved data source. The principle is to corroborate what appears on paper with connected data, then normalize both into one decision-ready file.

The outcome is not more data for its own sake. It is better evidence, formatted consistently, with fewer system toggles and clearer reason codes that speed decisions while preserving control.

For a practical primer, watch the live session on simplifying underwriting and read the companion article.

Borrower choice, lender control

Choice drives completion. Some applicants prefer to upload a pay stub. Others would rather tap “connect my bank.” Supporting both paths, then standardizing the evidence, raises completion rates without sacrificing governance. Underwriters, QA and compliance evaluate the same normalized features regardless of intake path, which improves consistency across channels and teams.

Where a unified model moves the needle

Products with fast funnels see the biggest lift: personal loans, credit cards, buy now, pay later and point-of-sale financing. The approach is especially effective with thin-file or near-prime applicants and borrowers with multiple income sources. Early in the process, mismatches surface quickly — for example, an employer on a pay stub that does not align with a connected employment response, or an ID image that fails a database check. Clean, consistent files move straight through. Exceptions route with context, which shortens queue time and limits second-look volume.

Fraud vigilance without extra friction

Evaluating uploads and connected data together makes sophisticated fraud harder to execute. Template reuse, synthetic identities and improbable activity are easier to spot when multiple evidence streams must agree. Reviewers can focus on the riskiest cases rather than touching every exception, which improves catch rates without adding steps for legitimate borrowers.

Risk, fairness and transparency

Speed only wins if decisions are explainable. A unified evidence model preserves lineage from source to extracted field to rule to decision, which supports fair lending, adverse action and audit readiness. Data minimization and security should be table stakes: collect only what is needed for a decision, protect it in transit and at rest, and monitor access. For broader consumer protection context, review guidance from the Consumer Financial Protection Bureau.

Book a demo today to learn how you can begin your docs + digital journey.

Key takeaways

- Support both uploads and permissioned connections, then normalize into one decision-ready file

- Unified evidence improves speed, reduces exceptions and raises fraud catch rates

- Clear lineage supports fair lending, adverse action and audit readiness

- Choice improves completion while preserving consistent underwriting standards